The Tax on Churn

Grant that a trading method has a small edge on paper. One last wall waits, and almost nobody clears it: tax. Moving realizes your gains; realizing means paying. A descriptive read — not tax advice.

The wall nobody clears

When a system moves in and out of a position at a gain, that gain is realized — booked, the position sold — and a realized gain is taxed straight away. The one who buys and holds realizes nothing until he sells: his tax is merely deferred, pushed to the very end.

In France, as of today, a flat 30% levy (the "prélèvement forfaitaire unique," or PFU) applies to capital gains realized in an ordinary brokerage account. As long as you don't sell, you don't pay it.

The difference looks like bookkeeping. It's decisive. Because the money you hand the taxman today no longer works for you tomorrow.

The patient one pays once, the restless one pays a thousand times

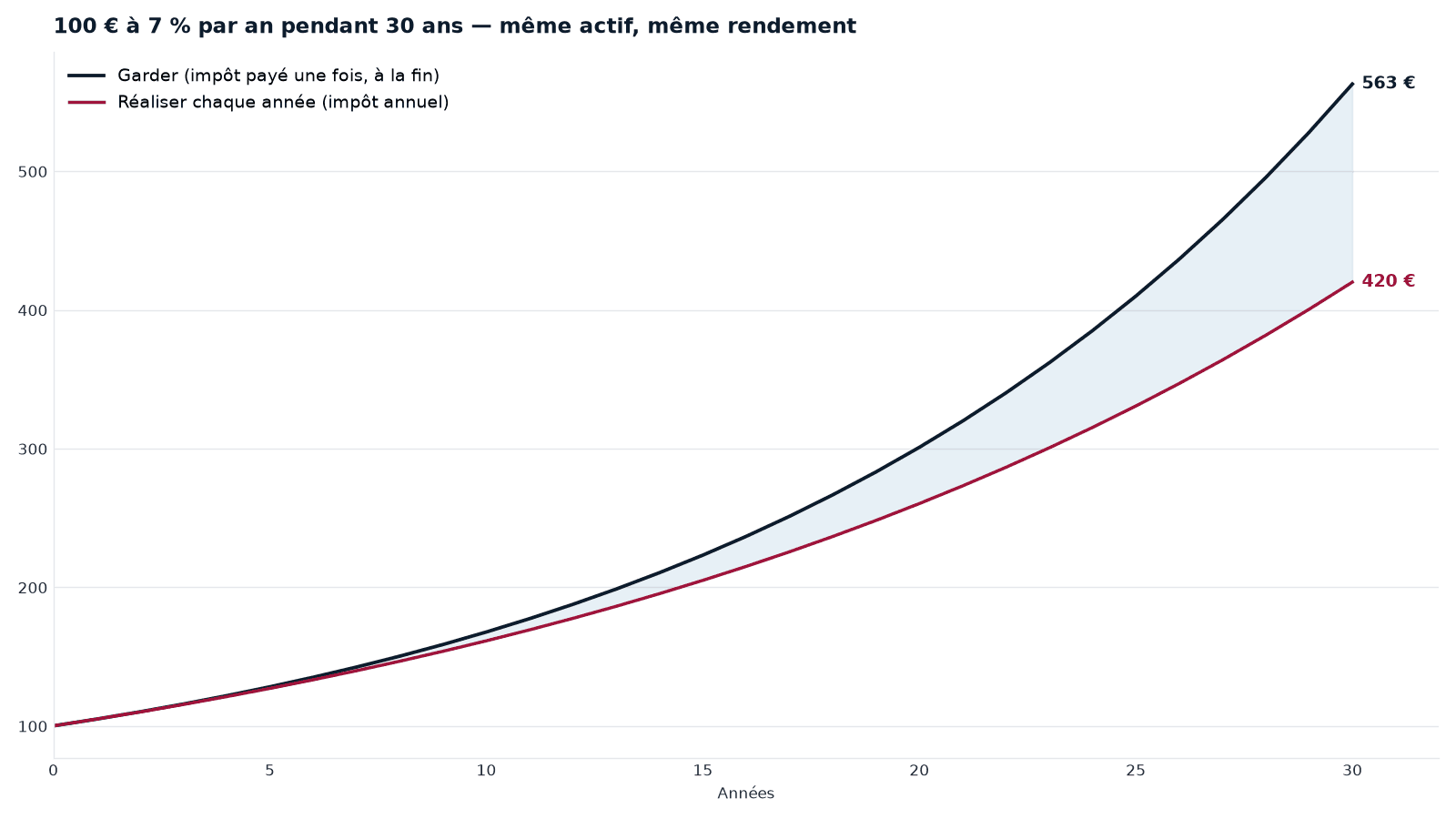

Picture two investors in the same asset, over thirty years. The first touches nothing: he'll pay his tax once, at exit, on the whole road traveled. The second moves in and out on a signal: at every gain booked, he pays his share — and carries on with what's left.

A textbook example, to see the difference (return assumed constant, for illustration — not a forecast): €100 invested for thirty years at the same return becomes €563 if you hold and pay tax only at the end — against €420 if you realize and pay every year. Same asset, same return; the only difference is when the tax lands.

And the gap widens with the horizon — the longer it runs, the more the money handed early to the taxman is missed:

| Horizon | Hold (net) | Realize every year (net) | Gap |

|---|---|---|---|

| 10 years | €168 | €161 | +4% |

| 20 years | €301 | €260 | +16% |

| 30 years | €563 | €420 | +34% |

Because the first puts a larger sum to work — his gains in turn produce gains — while the second's is forever whittled down. And it isn't the frequency of the round trips that matters most: it's the plain fact of realizing. Even a slow system, moving just once a year, books a hefty tax at every exit. Only pure deferral — never selling — escapes it.

A thin edge doesn't survive tax

Let's bring this mechanism back to the test bench. Before tax, the only edge the trend filters kept — the methods that follow the move — was risk-adjusted: a better ratio between gain and the jolts endured. In pure return, staying invested already led (see Ichimoku on the test bench). But these filters realize their gain at every exit. On a brokerage account, the drag we just saw is enough to carry off an edge this thin: buy-and-hold pulls back ahead on both counts.

And in our tests, the more often a strategy realized, the more tax took from it. By extension, the most heavily sold methods — day trading, rapid round trips — are the most exposed to this levy. The more you book, the more you pay.

The wrapper's irony

The container that holds your investments — a brokerage account (compte-titres), the PEA, life insurance (assurance vie) — each with its own tax rules. The same asset isn't taxed alike depending on the wrapper that shelters it.

The irony is complete. The only ground where you can truly automate active trading — the brokerage account, the one that directly allows borrowing to bet bigger, betting on the downside, buying and selling within the day — is also the one where the tax on churn bites hardest.

Conversely, the wrapper that does not tax round trips along the way — the PEA — shuts the door on direct speculative methods: no short selling to bet on the downside, no margin borrowing to stake more, no options or futures — the riskiest products. It makes a plain, measured back-and-forth between eligible funds viable by neutralizing the tax on movement — while shutting the door on the casino. The method that sells and the wrapper that tolerates it never meet.

What this reading does not do

This is neither tax advice nor investment advice. It doesn't say which wrapper to choose, nor what to buy, nor when to sell. It describes a mechanism — how the tax on realized gains weighs on strategies that realize often. Tax rules change and depend on each situation; the past does not predict the future.

Takeaways

- A realized gain is taxed straight away; the one who holds only defers his tax.

- It isn't mainly the frequency of trades that costs, it's the act of realizing: money handed to the taxman no longer compounds.

- On a brokerage account, the tax drag erases the edge — risk-adjusted only — that trend strategies kept before tax.

- The wrapper where active trading is possible (brokerage account) is the one that taxes it most; the one that spares round trips (PEA) shuts the door on direct active methods.

- Over time, the taxman rewards patience, not restlessness.

Go further

- Ichimoku on the test bench — what the backtest says about trading methods.

- Who really wins at trading — the house, the seller, the structural pro.

- The Cap Nord Manifesto — invest to endure, not to be right.

Discover Cap Nord

Method. The chart and table are an arithmetic illustration at a constant return (7%/yr) and the French flat tax (prélèvement forfaitaire unique, 30% as of today) on realized capital gains: they isolate the effect of when the tax lands alone — this is not a market backtest. The finding on trend filters (edge only risk-adjusted before tax, return led by "stay invested") comes from Cap Nord's internal study — see the Ichimoku article. A descriptive read, not tax advice; tax rules change and depend on each person's situation. The past does not predict the future.